Just a week after the long-rumoured mothballing of De Beers’ Snap Lake finally came to pass, and despite posting a 35 percent drop in sales for its third quarter ($145 million US, down from $222.5 million US last year), Dominion Diamond Corporation offered an optimistic take on the state of the diamond market last Friday.

“There have been some short-term headwinds,” Dominion president and CEO Brendan Bell said during a briefing on the report. “But looking back over the year, in terms of overall trends, rough diamonds have fallen about 8 percent but as an offset, the Canadian dollar has declined 20 percent.”

Bell claims that this has been a “transition” year for the company, which owns most of Ekati and a 40 percent share of Diavik. Despite the state of the market, development continues for Dominion, particularly at Ekati, the larger of the two mines.

There, production on the Misery line is set to begin again in the first quarter of next year, and a response from the Mackenzie Valley Land and Water Board is expected in January on the Jay pipe, which is said will extend the mine’s life into 2030.

The long and short term

Optimism or not, Dominion’s stock went on to hit their lowest prices in several years on Tuesday. But across the industry, several issues have driven diamond prices worryingly low, and the overarching question remains: is this a period of “transition” for the whole industry? And if so, what will it look like on the other side?

In the short term, there’s one immediately identifiable culprit: the slowing Chinese economy where overhyped demand has caused a supply glut. Dominion executive VP Jim Pounds spoke hopefully during the briefing of a potential resurgence in both Chinese and U.S. markets over the holiday season.

But the bigger concern for Northerners is the long-term market for the stones. Diamonds are an incredibly unusual commodity which has kept a high value through a mixture of both real and perceived rarity. Real in that De Beers’ long-held monopoly on diamonds kept the market undersupplied, and perceived in that De Beers has spent a fortune positioning diamonds as a precious “toll gate” to matrimony: a successful piece of social engineering they’ve pulled off in western countries since the 1930s, and one they are hoping to repeat in China.

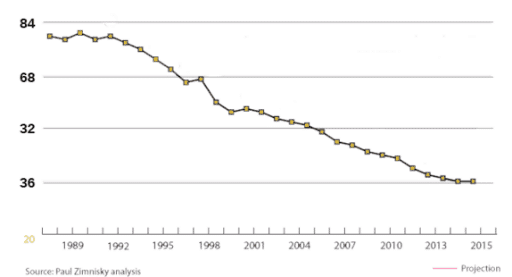

But since 1987, De Beers’ long-held monopoly and influence has steadily declined, thanks to the emergence of competitors and a major antitrust suit. Its share of the market has dropped from near 90 percent at its peak to just over 30 percent today.

Its monopoly allowed De Beers to set the price of diamonds for that whole industry, but that ability has steadily declined. Add to this, technological advancements which mean synthetic diamonds now make up 98 percent of industrial diamonds; although they have yet to make inroads into the jewelry market, they certainly have the potential.

The market and why it matters

Despite its decline of nearly 50 percent over the past decade, Peter Vician, deputy minister of Industry, Tourism and Investment has noted, it probably makes up 40 percent of GDP when directly related revenue, such as money spent on transportation and local businesses, is factored in.

Before the Snap Lake closure was made official, Tom Hoefer, executive director of the NWT and Nunavut Chamber of Mines, told EDGE the NWT is particularly vulnerable to the declining market.

“Our industry is a ‘price taker.’ In other words, we have to accept the price the market pays us for our goods,” he said.

The other concern for the local diamond industry is that diamonds are increasingly being mined elsewhere in the world, including other “blood-free” Canadian sites: De Beers’ operates a mine in Ontario, while new entrant Stornoway Diamonds is opening one in Quebec in 2017. And operating up here, even if the GNWT does invest in infrastructure such as roads, as industry advocates are asking for, is still bound to cost more than operations like Karowe in Botswana, where the second-largest diamond in history was just recovered.

The worst-case scenario for cutting costs, Hoefer said, is layoffs. For example, a large operator like De Beers’ parent company Anglo American has recently slashed 85,000 positions worldwide in response to the global drop in prices. Smaller operators like Dominion can also reduce the size of their operations and hope that “headwinds” will pass. But, as we have seen at Snap Lake, the mining industry often deals with low prices through temporary or permanent closure. Despite their optimistic words, this storm shows no sign of abating, and low prices as a new reality remain entirely possible. Ultimately, diamonds are just not as rare as mining operators would like, and stable demand in markets such as China is by no means a confirmed thing.

As diamond prices dropped following the last global financial crisis, Snap Lake shut down for a summer, a clear sign that it was likely the least profitable mining operation in the Northwest Territories. Now that diamond prices are again heading towards those lows, who will be next? Those with a long enough memory will remember that in that same summer Diavik was on the verge of a summer closedown shortly after as well. For everyone’s sake, let’s hope Dominion’s optimism is warranted.

With reporting from Elaine Anselmi